NORTH AMERICAN AUTOMOTIVE

From Site Selection magazine, January 2009

Honda Manufacturing of Alabama employees had a lot to celebrate in spring of 2008, when the first 2009 Honda Pilot SUV rolled off the line in Lincoln, Ala., where the company also produces the Odyssey minivan. In October, Honda said it would add yet another model to the high-performing plant's lineup.

Driving Forecast:

Cloudy

Cloudy

P

olitics does, indeed, make strange bedfellows. So do negative cash flows.

As the domestic auto industry continues to struggle, unusual alliances have formed: coalitions of suppliers, automotive dealers, the management of the Big Three domestic automakers and unions.

So precarious is the cash position of the domestic OEMs that everyone is trying to play nice, setting differences aside to rally for federal assistance.

The goal: nothing less than keeping Ford, General Motors and Chrysler alive as they struggle to pay bills, keep factory doors open and meet payrolls, at a time of diminished consumer demand and tight credit markets.

One such partnership – The Alliance for American Manufacturing – says that car makers' problems are rippling outward, impacting multiple related industries.

"Automakers are the largest customer of steel, aluminum, glass and other goods. If automakers are allowed to fail, the problems will impact every state in the nation," says AAM's executive director Scott Paul. His organization – an alliance between the United Steelworkers Union and management of Ford, General Motors and Chrysler – estimates a US$150-billion cost to the American economy if the domestic automakers fail.

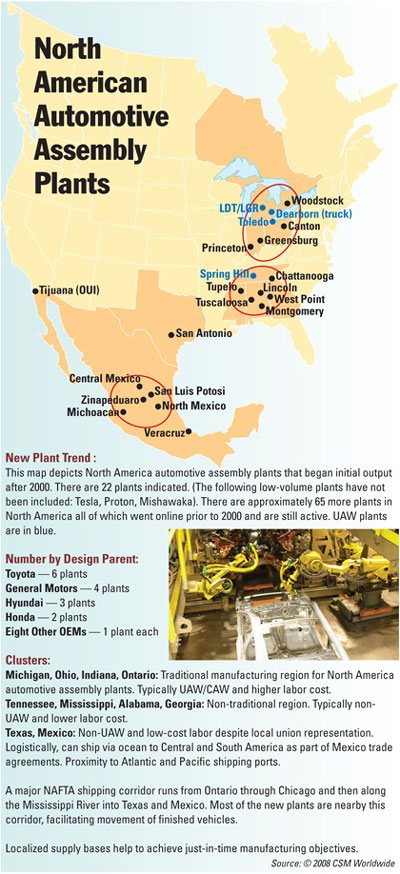

In fact, beneath the headlines, automotive location activity continues throughout the NAFTA zone. Recent location trends, such as a shift to Mexican production, are picking up speed. Other production-related trends, like platform consolidation, supplier diversification and green car manufacturing, are affecting location decisions going forward.

And the impact of multiple plant closings – six in 2008 alone, not including temporary retooling closures, with the likelihood of more shutdowns in the near future – remains to be seen.

Southeast and Westward Ho!

Now, these initial forays have become a groundswell, according to Vaughn Chapman, North American market analyst for CSM Worldwide.

"There might be a few new plants in the Michigan corridor, but it will not be a major trend in the future because it is an area of higher cost labor," he says. By contrast, there are seven new plants on line in the U.S. South, either slated for opening or just opened, in Tennessee, Georgia, Mississippi and Alabama." A prime reason, he says: "Lower cost wages and non-union facilities."

Union representatives suggest that concessions in recent years have made hourly wage comparisons more equitable, and that location scouts should think twice about moving away from the highly skilled automotive labor pool of the heartland because these gaps will close for newly hired workers.

"The union has made extraordinary concessions," notes Paul, of AAM. "Ultimately, the cost structure of union plants will be lower on wages and benefits compared to the domestic operations of foreign automakers."

But others say that a head-to-head hourly wage comparison does not get at the heart of the issue.

"It isn't always about the hourly wage," says Gregg Wassmansdorf, who oversees the location advisory and incentives practice for Colliers International. "It's also about flexibility."

In a union shop, managers sometimes are restricted from deploying workers as needed. "Union workers in certain job categories are not contractually able to do other things. So you might not be able to move a worker to another part of the plant to help with a backlog," Wassmansdorf notes. This can have a significant negative impact on productivity, while adding to operational costs.

Changing demographics are playing a role in the geographical shift as well.

"The Southeast and West have some of the fastest growing population centers in North America," says Chapman. "This is where demand will be greatest as the economy picks up again – not in the Midwest, which is losing population rapidly."

Adds Wassmansdorf, "Mathematically, there are many more vehicles being made in the Midwest than there is population to buy them."

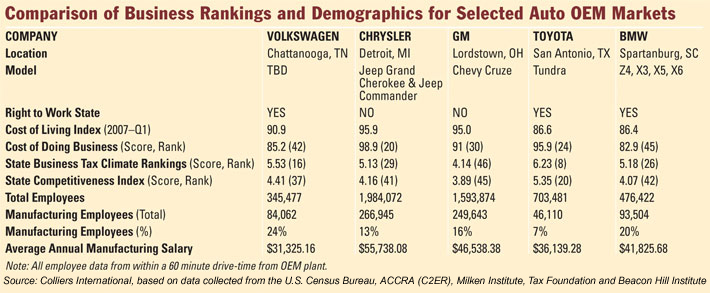

The biggest announcements in the OEM world this year bear out this continuing shift away from the North American heartland. In July, Volkswagen determined that it would redevelop a shuttered military base in Chattanooga, a $973.5 million investment to produce 150,000 cars annually, after an intensely competitive site search that included Michigan, Alabama, North Carolina and South Carolina. BMW is expanding in the South as well. The company is investing an additional $750 million in its Spartanburg, S.C., campus to add 1.5 million sq. ft. (139,350 sq. m.) and 500 new jobs, with a goal of increasing production capacity to 240,000 units by 2012.The company will build a new 1.2 million-sq.-ft. (111,480-sq.-m.) plant due north of the existing factory, as the global production site for its new BMW X3 Sports Activity Vehicle.

Toyota is growing its presence in the South as well, although the nature of the growth has changed dramatically in the last year. In 2007, the company announced plans to build more of its Highlander SUV at a new facility on 1,700 acres (688 hectares) in Blue Springs, Miss. In July 2008, with demand for trucks declining, the company said it would configure the $1.3-billion plant for domestic production of its popular hybrid Prius, currently an import.

Tex/Mex Appeal Grows

"Under a new administration, there could be changes that would enable union penetration into facilities in the South," Chapman observes. "This could make Mexico even more attractive for automakers."

One change that the new Congress could consider – passage of the Employee Free Choice Act. EFCA would essentially make it easier for workers to authorize union representation in a non-union workplace, by replacing the current several-step, secret ballot process with a "card check," whereby workers sign cards indicating their support for unionization in the presence of fellow employees and union organizers. Under the proposal, if a majority of workers sign the cards, the union is authorized.

Without the union issue to contend with, and generally lower operating costs, OEMs and suppliers alike are finding plenty to like in Mexico. According to Mexican economic development officials, Chrysler will shift much of its design work away from the U.S. to Mexico City and to China, for an estimated 40 percent product design cost savings. Daimler is building a heavy truck plant for its Freightliner division in Saltillo. Nearby, a new Chrysler engine plant will open its doors in 2009.

And, financial troubles aside, GM is pinning its future hopes on a new Mexican plant that will manufacture its all-electric Chevy Volt, slated to roll off the assembly line in 2010. The new facility in San Luis Potosi is adding to an emerging automotive cluster in central Mexico.

Changing Dynamics: Suppliers Take Control of Location Decisions

"Suppliers tried to create a facility everywhere an OEM told them to," Wassmansdorf says. "But this has become too expensive. They can't be as efficient or provide the price givebacks OEMs want by building more facilities."

Increasingly, suppliers are consolidating operations, shutting down underperforming facilities and ramping up production at others.

"Tier One suppliers are saying that they will group customer requirements at the same facility," Wassmansdorf says. "They are telling OEMs that their parts production will share the same facility, and that they can be served just as efficiently from an existing facility, six hours away," rather than building a new plant or keeping an underutilized plant in operation.

MAHLE is consolidating production at this facility in St. Johns, Mich. Though the company is expanding at another plant in Aguascalientes, Mexico, St. Johns won out for the consolidation over sites in Mexico and Brazil.

"The reality is that the expansion in St. Johns is a consolidation of the business," says MAHLE spokesperson Jeff Trent. "We are moving all of our U.S. customers under one roof."

The St. Johns facility houses both MAHLE, which supplies the Big Three, and the company's joint venture with Riken Corporation, Allied Ring Corp., supplier to transplants Toyota, Nissan and Honda. St. Johns won out over sites in Brazil and Mexico, in part by sweetening the pot with $3.8 million of incentives, including a $2.2-million, 12-year state tax credit.

Other suppliers, such as Timken, are diversifying as a hedge against automotive cycles. Even as the company opens a $60-million, small-bar steel rolling mill in Canton, Ohio, to supply its automotive customers, the firm continues to move away from automotive products, expanding its portfolio of differentiated steel products for a range of industries.

"We are focusing only on automotive product lines where we have unique capabilities," says Timken spokesperson Lorrie Paul Crum. The new Ohio mill will produce tiny, high-performance steel bars for use in power transmissions – and in other friction management applications.

"For us, the best future is to be diversified," Crum explains. "We now supply a number of industries so we can smooth out single market cycles and shift production if demand falls in one industry and rises in another." The only growth projected for the company's automotive business is with the transplants – not with the Big Three, she adds.

As part of this strategic shift, the company has overhauled its structure and consolidated platforms. Plants like Timken's automotive facility in Honea Path, S.C., are retooling to produce products for multiple industries. Today, the South Carolina plant also produces landing gear for 737s.

Could Search for Value Could Send Industry Back North?

As the industry looks beyond the current gloom, it will continue to search for the best value. Some analysts are suggesting that in this search for value, the Midwest could start to look attractive again.

"There will be industrial assets available at 25 cents on the dollar," notes Wassmansdorf. "The combination of cheap real estate and a skilled but underemployed work force prepared to make a deal on wages in places like northern Ohio could make things more interesting from a location perspective down the road."

It's a bit too soon to tell whether states hard hit by automotive losses will beef up incentives to try to win back lost business. "A lot of these states are fiscally tight. While more incentives would be logical, they could be tough to deliver," Wassmansdorf says.

And, like their suppliers, OEMs are finding value in consolidating platforms under fewer roofs. Toyota's recently completed expansion of its Georgetown, Ky., plant allows production of its new five-seater, the Venza, on the same assembly line with the Camry, Camry Hybrid and Solara convertible.

This could mean additional growth in place for some companies, as they increase production at some plants while closing others. GM has signaled its intent to shutter nine more manufacturing facilities in the near future. Other car makers could follow suit.

As manufacturers consolidate production into fewer facilities, they also are leveraging North American manufacturing capabilities for export to other markets, as BMW is doing in South Carolina.

In October 2008, Toyota announced its intent to export Tundras from its San Antonio facility to burgeoning Latin American markets – up to 1,000 trucks a year. Plans also include exporting 15,000 Sequoia trucks annually from the Princeton, Ind., plant to cash-flush consumer markets in the Middle East. Sequoia exports to the Middle East are forecast at approximately 15,000 units annually.

On the Horizon: Facilities Aftermarket Boom; Greenfields for Green Cars

"Existing facilities aren't necessarily assets. What do you do with an old automotive plant?" Wassmansdorf notes. Developers and localities are trying to be creative, as they have been in envisioning new uses for military bases closed under BRAC guidelines. "We are seeing a trend toward converting plants into mixed-use projects, and breaking sites into smaller chunks for use as business incubators or warehouse space," says Wassmansdorf.

Duke Realty has taken on such a challenge, as it remediates and redevelops a decommissioned General Motors plant in Baltimore for a mixed industrial and commercial project, including distribution facilities, research and office space. Similar proposals are on the table in Atlanta, where both Ford and GM have just closed plants.

In some cases, companies are holding on to the assets, as Ford is doing with its Michigan Truck Plant, which closed in November 2008, and will re-open in 2010 as a factory producing small, fuel-efficient cars.

Another trend to watch: more groundbreakings for electric car producers as the industry retools for fuel efficiency. Still, some recent projects have been put on hold because of financial problems, such as a Kentucky's much publicized deal with low-speed, three-wheeled electric car maker ZAP. The state endorsed a $48-million incentives package for the project, a joint venture with Integrity Manufacturing on a 225-acre (91-hectare) site in an industrial park in the city of Franklin. Now, the project has stalled, and parties involved appear uncertain as to if – or when – the plant will be built. "I don't know the status of the project," says ZAP spokesperson Alex Campbell.

"Our understanding is that they are having difficulty securing financing," says J. R. Wilhite, Kentucky's commissioner for new business development.

In these uncertain times, it's not an unusual story.

Site Selection Online – The magazine of Corporate Real Estate Strategy and Area Economic Development.

©2009 Conway Data, Inc. All rights reserved. SiteNet data is from many sources and not warranted to be accurate or current.

©2009 Conway Data, Inc. All rights reserved. SiteNet data is from many sources and not warranted to be accurate or current.